Markets

Trading Hours

Wall Street Prepares for Around-the-Clock Stock Market

12/16/202512/16/2025

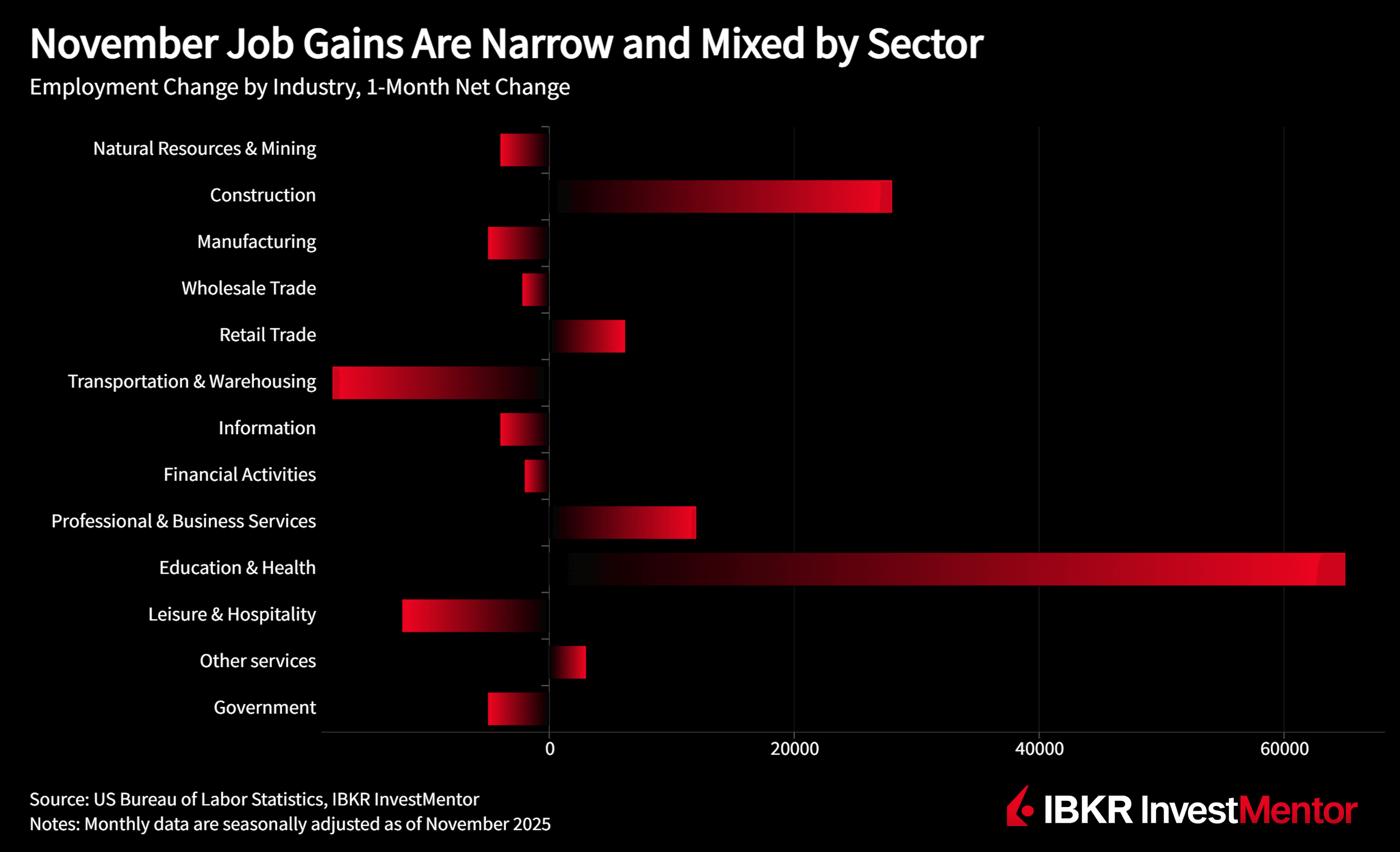

Total nonfarm payrolls rose by just 64,000 in November and have shown “little net change” since April. That’s a very different backdrop from the rapid job gains we saw coming out of the pandemic. Hiring is still positive, but we’re much closer to stall speed than to a booming labor market.

The gains that did show up were narrow:

Offsetting that, we saw:

The unemployment rate held at 4.6%, little changed from September, but up from 4.2% a year ago. That translates to 7.8 million people unemployed, versus 7.1 million last November.

Under the surface:

One number that stands out: people working part time for economic reasons jumped by 909,000 to 5.5 million. These are workers who want full-time jobs but can’t get the hours. That’s often an early sign that employers are trimming at the margins, cutting hours before cutting heads.

Average hourly earnings for all private workers rose just 0.1% on the month and 3.5% over the past year. For production and nonsupervisory workers, pay was a bit stronger (+0.3% m/m), but we’re still well below the peak wage growth seen earlier in the cycle.

The average workweek ticked up slightly to 34.3 hours, but manufacturing hours and overtime were basically unchanged. Taken together with the rise in involuntary part-time work, this still looks like a labor market where bargaining power is drifting back toward employers.

The report is also complicated by the federal government shutdown that ran from October 1 to November 12:

Even allowing for that noise, the broader pattern is clear: job growth has downshifted, unemployment is higher than a year ago, and under-the-surface slack (short-term unemployed, involuntary part-time) is building gradually.

For policymakers and markets, this print supports the narrative of a slow-cooling labor market rather than a sudden break:

For investors, the takeaway is that the “late-cycle” feel of the economy is now showing up more plainly in the data: narrow sectoral job gains, softer payroll growth, still-positive but moderating wages, and more people settling for fewer hours than they’d like.

Want to explore more? Download our free app to unlock expert news updates and interactive lessons about the financial world.