Markets

Defense Rally

Why Defense Stocks Keep Making Headlines

1/8/20261/9/2026

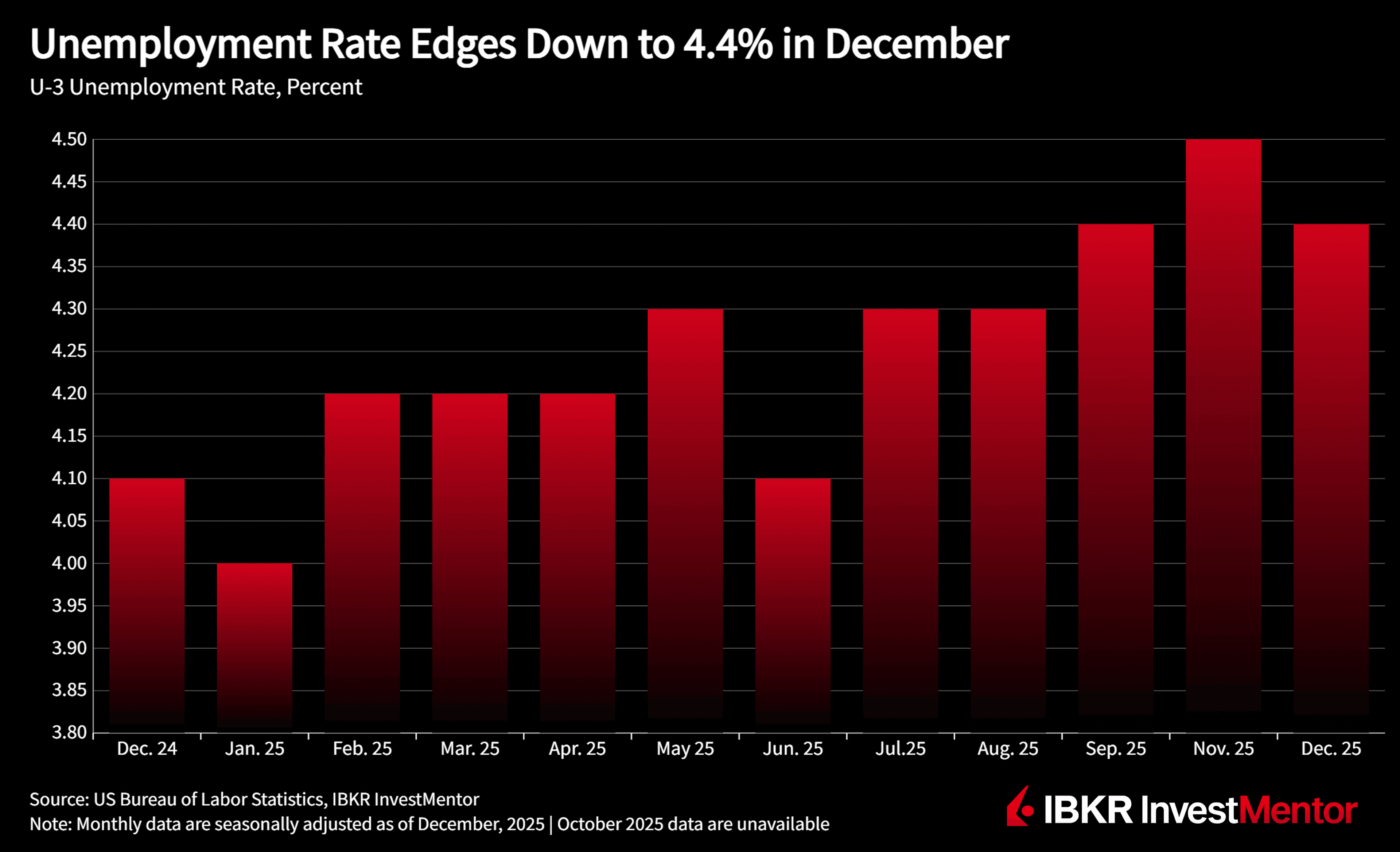

December’s data tell a story of a labor market that looks stable on the surface but is carrying more pressure underneath. The unemployment rate improved to 4.4%, even after seasonal revisions lifted earlier readings, and payrolls rose modestly by 50,000 jobs. On paper, that’s not a weak market. But when you line it up alongside underemployment, long-term joblessness, wages, and sentiment, you see an economy that feels a lot tougher to households than the headline suggests.

From the household survey:

Revisions to past data mean this 4.4% reading now represents a clear improvement from where the jobless rate had been tracking earlier in 2025. By age and gender, unemployment for adult men and women sits at 3.9%, and 15.7% for teenagers, with little change over the month.

But several “quality-of-labor-market” indicators are moving in a more worrying direction:

Labor force participation (62.4%) and the employment–population ratio (59.7%) have barely moved all year.

On the establishment side:

The gains are narrow and familiar:

Those sectors speak to steady demand for services and care, not a broad hiring wave.

Retail trade lost 25,000 jobs, with declines at warehouse clubs/supercenters and food & beverage retailers, partially offset by gains at electronics and appliance stores. Federal government employment was flat on the month but down 277,000 (9.2%) since January, as prior expansions unwind.

Revisions added a sour note:

Together, that’s 76,000 fewer jobs than first reported, reinforcing the sense that momentum has already been fading for a while.

Pay is still rising, but not enough for workers to feel relaxed about their finances:

So, households see solid wage growth on paper, but two things blunt the comfort:

The latest consumer sentiment data underline that:

Put all of this together and the narrative isn’t “everything is fine” or “everything is breaking.” It’s more nuanced:

It’s a labor market under quiet pressure: still functioning, still creating jobs, but delivering a day-to-day reality that feels tight for many households. For policymakers, that mix complicates the calculus—on one hand, there’s no clear collapse to force immediate action; on the other, there’s little sign that workers feel like they’re back in a genuinely comfortable spot.

Want to explore more? Download our free app to unlock expert news updates and interactive lessons about the financial world.