Markets

Anthropic IPO

Anthropic's Listing Tests the “AI Bubble” Theory

6/3/20266/4/2026

Investors are trying to pull billions out of private credit. US giant Blackstone revealed that so many people wanted out of its BCRED fund that it chose not to fulfill all requests. Before this quarter, Blackstone was one of the few funds that still fulfilled all withdrawal requests.

Most private credit funds don’t trade like stocks. Typically, you can request withdrawing money only once every quarter, and there’s a limit, usually 5% of the fund’s total assets, on how much money can leave at once.

In this case:

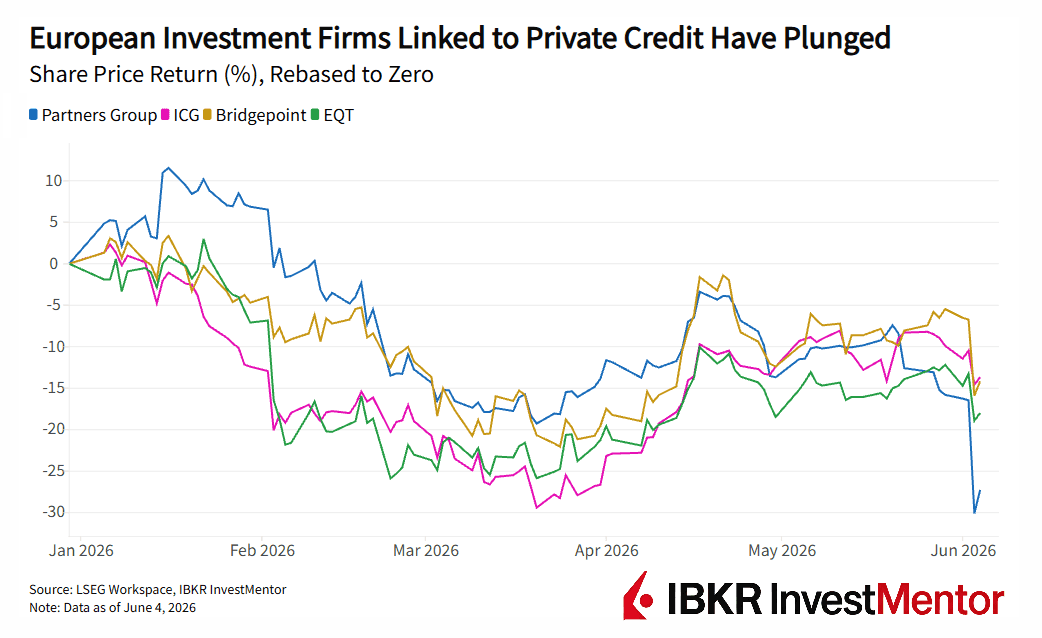

Blackstone’s move followed the news of Swiss private lender, Partners Group, capping a fund aimed at wealthy individuals. The company warned that another one of its funds would soon be capped too, with potentially more to come.

This was particularly concerning as the fund was marketing to retail investors, not institutions. Rival Cliffwater announced similar limitations on its retail clients' fund just a day before.

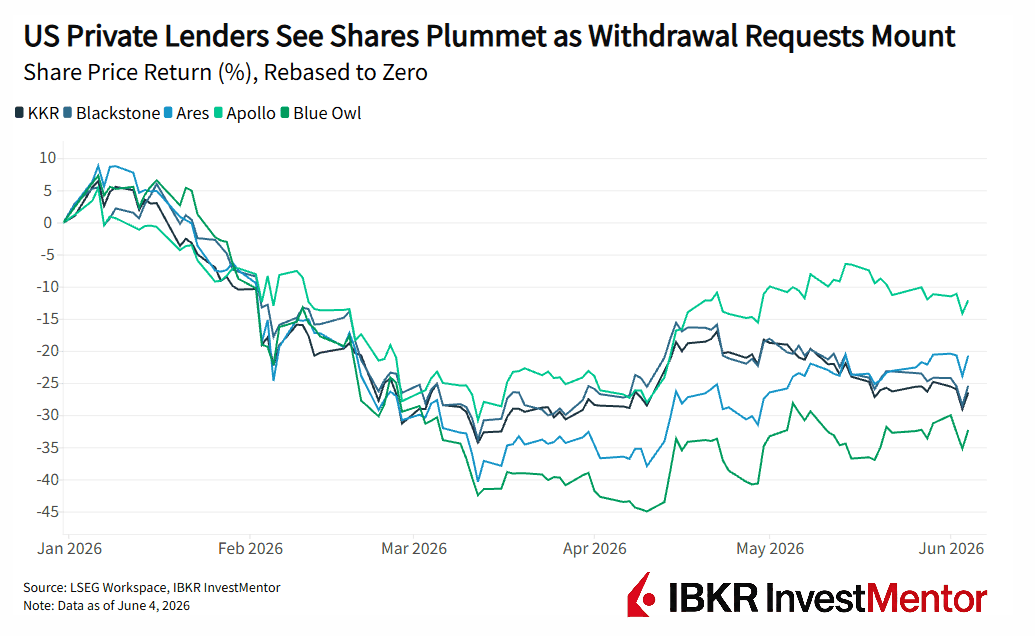

This redemption pressure is rising across private lending in both the US and Europe. American heavy-hitters like Blue Owl, Apollo, and Ares have all done similar moves before.

Private credit is money lent to companies by non‑banks: investment funds, pension funds, and specialist lenders like Blackstone and Partners Group.

Deals usually come with flexible terms and higher interest rates, accounting for more risk. After the 2008 financial crisis, banks tightened their purse strings, so private lenders stepped in. It has become essential for small and medium-sized firms that struggle to get bank loans.

Once niche, private credit has exploded. At the end of 2025, it had $3.5 trillion assets under management. But there’s very little visibility on the quality of these assets, fueling fears about contagion.

These types of funds invest in assets that take time to sell. Private credit funds lend to companies. Private equity funds own stakes in businesses. Neither can be liquidated quickly without taking losses.

To avoid that, managers cap how much money can leave each quarter. This protects remaining investors from forced sales. But it comes with a trade-off:

The system works smoothly in calm markets. The strain shows when many investors try to exit at once. That’s exactly why these limits exist — to keep the fund stable when confidence drops.

Markets reacted immediately to the news of Partner Group's withdrawal caps, with shares falling across the industry on Wednesday.

But Thursday saw many of the same names ticking up, with Blackstone actually surging 8%. This was because, despite capping withdrawals, Blackstone flagged that requests have reduced, markets are stabilizing, and its BCRED fund has actually delivered 11% profits over the past 12 months.

This calmed the markets somewhat, but private lender stocks have been volatile for months now, with investors questioning the quality of the underlying assets.

The pressure partly traces back to the AI boom. Many private credit funds financed software and enterprise tech companies, including firms exposed to building data centers and renting out high-end chips. They also have big bets in software companies.

Partners Group, for example, disclosed that some of its largest holdings are in technology.

European Central Bank warned in May that private credit-fueled AI boom could pose a risk to the financial system, especially if AI demand falters. ECB estimated that Eurozone pension funds could lose 5-6% of their value in a “severe shock” to the private credit market.

Want to explore more? Download our free app to unlock expert news updates and interactive lessons about the financial world.