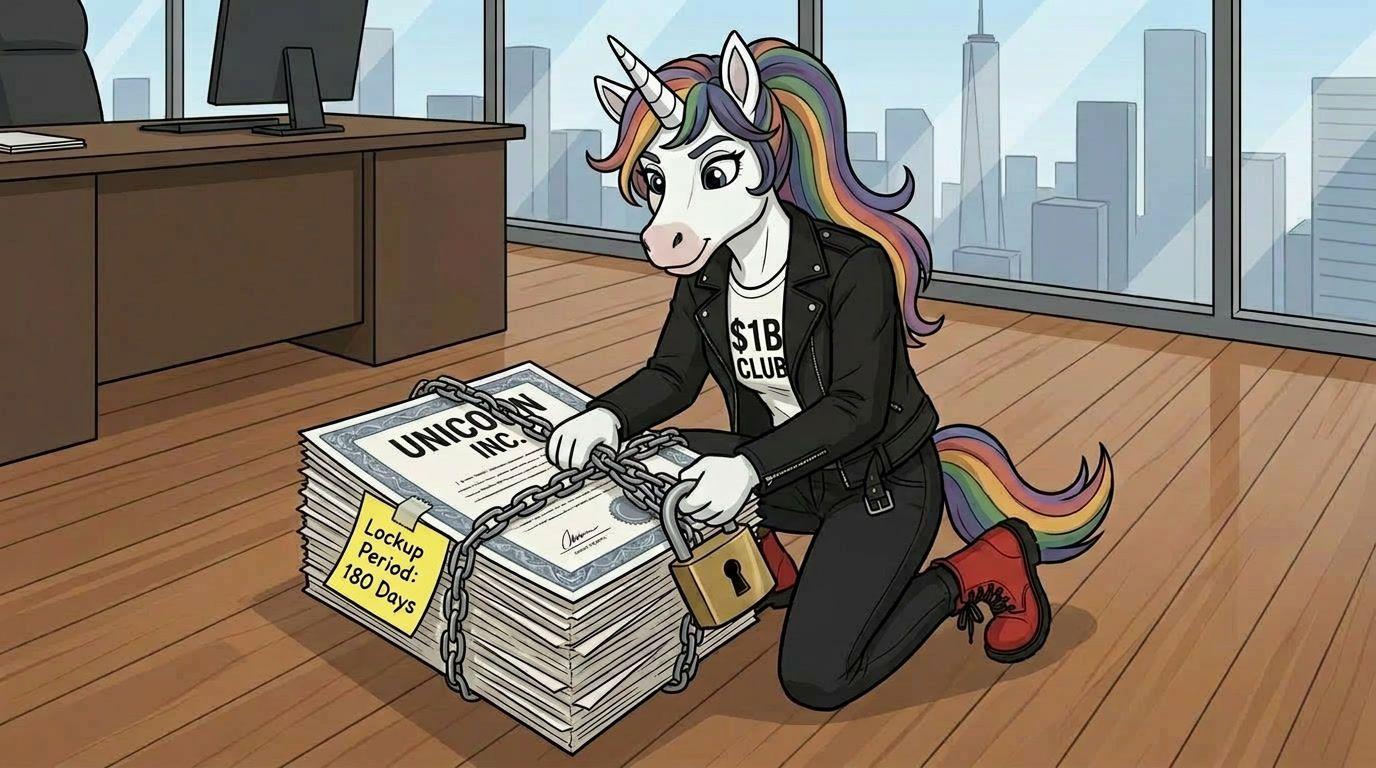

Lockup Period

What Is It?

You work at a Silicon valley tech company that’s preparing its initial public offering (IPO). The company starts trading on Nasdaq, the stock rockets — and you can't sell a single share. Welcome to the lockup period.

When a company lists on a stock exchange, insiders are usually banned from flooding the market right after the IPO. This commonly includes founders, early investors, and employees.

In the US, the standard lockup lasts 180 days. It’s not legally required, but most IPOs still have them to build trust among investors. Some countries, like China and South Korea, use mandatory lock-up periods.

Why Should I Care?

Because lockup expiry dates move stock prices. Food company Beyond Meat collapsed as much as 24 percent back in 2019 as its 180-day lockup ended and 75% of outstanding shares hit the market. Not every insider sells immediately, but a sudden jump in supply tends to push share prices lower.

And the rules are getting more complex:

- Staggered releases let insiders sell in tranches, not all at once

- Performance triggers unlock shares early if the stock hits a target price first

- Founders may face longer restrictions, sometimes double the standard period

What’s the Catch?

Retail investors often forget to keep track of lockup periods, and it’s becoming even more difficult with staggered contracts. They sound investor-friendly: no sudden flood of shares. But they also extend the uncertainty window and obscure the real supply.

These structures also reflect a power shift. The 180-day lockup was long a market standard, imposed by underwriting banks to stabilize newly listed stocks. Now, some companies are powerful enough to set their own terms. Airbnb, DoorDash, and Snowflake all secured early releases, while SpaceX’s record-breaking 2026 IPO used a multi-step schedule, with the free float rising gradually from about 5% to nearly 100% within a year.